اعتباری چیست؟! 5C

چنانچه شما صاحب یک کسب و کار کوچک هستید ، آیا می دانید چگونه می توانید شانس خود را در دریافت وام از موسسات مالی و اعتباری بالا ببرید.؟ بهترین راه برای انجام این کار آشنایی با 5C خواهد بود. دانستن اینکه 5C چیست ، چگونه کار می کنند و چرا مهم هستند و می توانند شانس شما را برای دریافت تسهیلات از موسسات مالی و اعتباری بالا ببرد.

به عبارت ساده ، 5C چارچوبی است که تعداد زیادی از موسسات مالی و اعتباری به صورت سنتی از آن بهره می گیرند تا در بررسی درخواست تسهیلات مشتریان از آنها استفاده کنند.

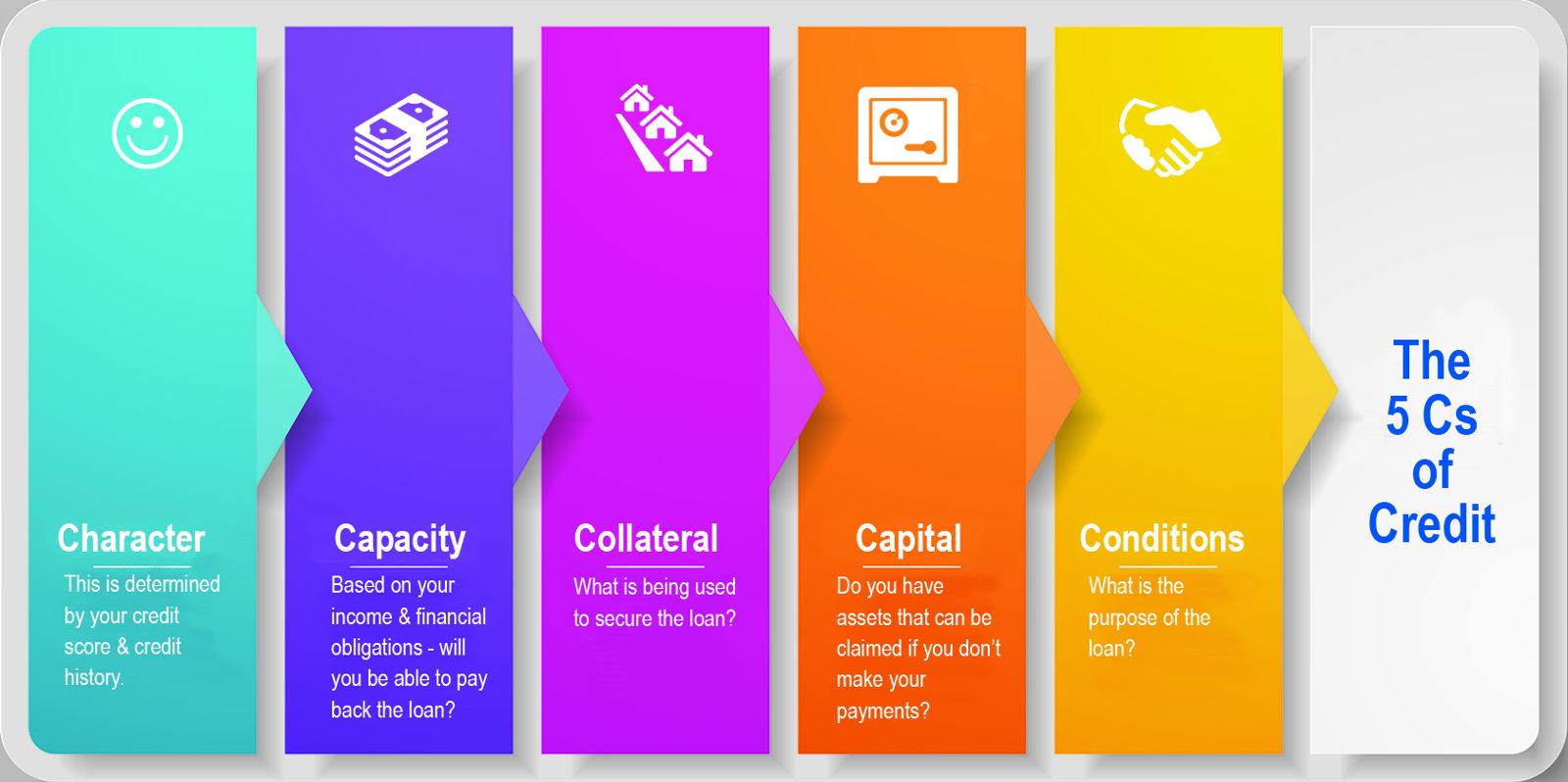

5C در واقع مخف شخصیت ظرفیت سرمایه شرایط وثیقه است

Character |

Capacity |

Collateral |

Capital |

Conditions |

1.شخصیت

این شاخص با تکیه بر بررسی ابعاد شخصیتی درخواست کننده وام به عنوان یک فرد به طور مستقل با تکیه کمتر بر جوانب کسب و کار افراد. به این موضوع می پردازد که آیا فرد درخواست کننده دارای آیتم های مثبت شخصیتی برای دریافت تسهیلات هست یا خیر برای موسسات مالی ارائه کننده تسهیلات بسیار مه خواهد بود که بدانند شما از نظر شخصیتی تا چه حد قابل اعتماد خواهید بود . آیا بر سر قول خود برای بازپرداخت به موقع اقساط خواهید ماند .؟ بهترین راه برای کسب این آیتم ، ایجاد ارتباط و تعامل با بانک یا موسسه اعتباری محل زندگی یا فعالیت اقتصادی شما خواهد بود .یک گام به جلو بردارید و با بانکداران ملاقات کنید و ببینید که آیا می توان با ایشان یک رابطه کاری برد برد برقرار نمود.

2. ظرفیت

این شاخص بیانگر توانایی کلی شما برای بازپرداخت وام مورد نظر است. بر کسی پوشیده نیست که چرا این امر برای موسسات مالی که به شما وام می دهند مهم است. زندگی و حیات اقتصادی آنها به باز پرداخت اقساط شما وابسته خواهد بود.موسسات مالی ظرفیت شما را تقریباً کاملاً بر اساس تاریخچه مالی شما ارزیابی می کنند. این شامل تاریخچه شما برای وام و بازپرداخت وامهایی است که در گذشته گرفته اید ، نمره اعتباری خود و سایر معیارها مانند نسبت بدهی به نقدینگی و صورت جریان وجوه نقد از کسب و کار شما. بهترین راه برای کسب این آیتم ، پرداخت حداکثر بدهی خود قبل از درخواست وام جدید است. یک گام دیگر به جلو بردارید و با بازپرداخت به موقع تسهیلات دریافتی قبلی نمره اعتباری خود را بهبود ببخشید.

3. سرمایه

این شاخص بیانگر مقدار پولی است که درکسب و کار خود سرمایه گذاری کرده اید. موسسات مالی اغلب دوست دارند ببینند كه صاحبان مشاغل همانطور كه ادعا می کنند فقط اهل حرف نبوده و مرد میدان عمل خواهند بود .! این بدان معنی است که آنها دوست دارند افرادی را ببینند که پول خوبی را در کسب و کار خود سرمایه گذاری کرده اند ، و قصد آنها از درخواست تسهیلات فقط تامین سرمایه اولیه نخواهد بود. یک موسسه مالی از گزارش های مالی شرکت شما برای ارزیابی سرمایه شما استفاده می کند. آنها قادر خواهند بود تا ببینند مبلغی كه در ابتدا به این كسب و كار سرمایه گذاری كرده اید و آیا از آن زمان پول اضافی را وارد كسب و كار كرده اید یا خیر. بهترین راه برای کسب این آیتم ، ایجاد سرمایه در گردش مناسب و در خور کسب و کار شما خواهد بود.یک گام دیگر به جلو بردارید داشتن سرمایه در گردش امری بسیار حائز اهمیت خواهد بود.

4. شرایط

این شاخص بیانگر 2 موضوع خواهد بود. اول : ما در مورد وضعیت شغل خود صحبت می کنیم - این که آیا تجارت شما به خوبی پیش می رود یا خیر ، و همچنین اینکه چرا می خواهید از وام استفاده کنید و قصد شما از دریافت تسهیلات چیست. دوم : ما درمورد شرایط کلی پیرامون شما صحبت می کنیم - وضعیت صنعت شما نسبت به شاخص کل ، وضعیت کلی اقتصاد و چگونگی تأثیر هر یک از این موارد در تجارت و توانایی بازپرداخت شما.مؤسسات مالی در نهایت می خواهند به افرادی که در شرایط خوبی قرار دارند وام دهند. هر چه شرایط پیرامون آن فرد بهتر باشد ، احتمال بازپرداخت وام در هر شرایط احتمال بیشتری دارد. موسسات مالی با ارزیابی کلی اقتصاد ، نحوه انجام کار شما در مقایسه با صنعت عمومی و یا رقبا و روابط شما با مشتریان و تأمین کنندگان ، این ارزیابی را انجام می دهند.برخی از این شرایط کاملاً خارج از کنترل شما خواهد بود. بهترین راه برای کسب این آیتم ، این است که کسب و کار خود را بهبود بخشیده و در زمانی که در وضیت خوبی هستید اقدام به درخواست تسهیلات نمایید. یک گام دیگر به جلو بروید بهترین زمان برای دریافت تسهیلات نقطه اوج کسب و کار شماست.

5. وثیقه

این شاخص بیانگر آن بخش از دارایی شماست که برای تأمین یا تضمین وام مورد نظر خود استفاده می کنید. مؤسسات مالی ممکن است در صورت نیاز به گرفتن وام ، انواع مختلف وثیقه را در نظر بگیرند. این می تواند تجهیزات تجاری یا املاک و مستغلات شما باشد. این می تواند سرمایه در گردش شما باشد که شامل موجودی و حساب های دریافتنی شما باشد. حتی می تواند خانه شما باشد.بهترین راه برای کسب این آیتم ، وام دهنده ای را انتخاب کنید که نیازی به وثیقه های سنگین نداشته باشد و نرخ بهره آن برای جبران فقدان ضمانت معقول باشد. این آخرین گام برای شما ست تا به تسهیلات درخواستی خود دست پیدا نمایید.

منبع :

https://www.caminofinancial.com/what-are-the-5-cs-of-credit/

As a small business owner, you know how important it is to put yourself in the best position to receive funding from financial institutions, but did you know that the best way to do so is by mastering the 5 C’s of credit? Understanding what the 5 C’s of credit are, how they work and why they’re important can put you in the best position possible to receive funding for your business when you need it.

Very simply put, the 5 C’s of credit is a concept or a framework that a large number of traditional lenders will use as part of their evaluation of small business borrowers. Each of the 5 C’s actually stands for a characteristic of a person’s creditworthiness — character, capacity, capital, conditions, and collateral.

While there isn’t a hard-and-fast rule when it comes to exactly what you need in each of these characteristics — since different lenders require different things — following the basics of the 5 C’s of credit will help put you in the best position possible when you’re looking to obtain funding for your business.

1. Character

In terms of the 5 C’s of credit, the character is how a lender will view you from a personality, credibility and trustworthiness standpoint. This is more of a determination of your character as an individual, and less about certain aspects of your business.

Your personal character is important because financial institutions desire clients who are trustworthy, will keep their word and, ultimately, will pay back their loans on time. They assess your character through things such as your credit history, references and any reputation/interaction you’ve had with other lenders.

The best way to master the C of character is to establish a relationship with your local community bank or financial institution that you hope to do business with. Meet the local banker who’s in charge of business banking and see if you can establish a working relationship that benefits both you and them.

2. Capacity

Capacity represents your general ability to repay the loan that you are taking. It’s no secret as to why this would be important to financial institutions that are lending you money. They only make money if you keep up your end of the bargain and pay back the loan you took.

Financial institutions will assess your capacity based almost entirely on your financial history. This includes your history for borrowing and repaying loans you’ve taken in the past, your credit score and other metrics such as your debt-to-liquidity ratio and cash flow statements from your business.

One of the best ways to master this C is to pay down your debt as much as possible before applying for a new loan. This will improve almost all aspects of your capacity, including your cash flow, credit score and borrowing history.

3. Capital

Capital in terms of the 5 C’s of credit is the amount of money that you have invested in your business. Financial institutions often like to see that business owners have “skin in the game, ” as they say. What this means is they like to see people who have invested a good chunk of their own money into their business venture, and didn’t just borrow the money to get it started.

A financial institution will use your business’ financial reports to assess your capital. They’ll be able to see how much money you invested into the business originally and whether you pumped any extra money into the business since then.

An easy way to master this characteristic is to obviously invest at least some of your own money into the business. Beyond this, though, it’ll be important that you keep good records that show what your investments into the business were and what your working capital is.

4. Conditions

Conditions in the realm of the 5 C’s of credit refers to two things, actually. First, we are talking about the condition of your business itself — whether your business is doing well or not, as well as what your intended use of the loan is or how much you intend to borrow. Second, we’re talking about the general conditions around you — the state of your industry, the state of the overall economy and how each of these may affect your business and your repayment ability.

Financial institutions ultimately want to lend money to people who are in good condition. The better the conditions surrounding that person, the more likely he or she is to repay the loan per the terms. Financial institutions will make this assessment by reviewing the overall economy, how your business is doing compared to your general industry and/or competitors, and your relationships with both customers and suppliers.

Some of these conditions will be completely out of your control. For example, there’s little you can do to influence the state of the overall economy in the United States. However, you can control the conditions regarding your business. You should apply for a business loan when your business conditions are good — when your business is performing well and when you as an individual have good financial metrics.

5. Collateral

Collateral refers to any assets that you have that you will use to secure or guarantee the loan for which you are applying. Collateral will be used as a form of repayment on the loan if you can’t repay it the traditional way.

Financial institutions may consider a number of different types of collateral if they require it from you to take a loan. This could be business equipment or real estate that you own. It could be your working capital, which would include your inventory and accounts receivable. It could even be the home that you own.

To master this C, it’s important to choose a lender that doesn’t require collateral and whose interest rates to compensate the lack of guarantee are still reasonable. You want to protect your most valuable personal assets should the unfortunate time come when you have trouble repaying a loan. The last thing you want to do is open yourself up to having your home or other properties seized because you fell on hard times with your business.